Client Login

Client Login Contact

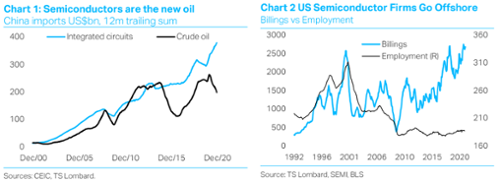

ContactThe structural shift in demand for semiconductors moves the focus of global geopolitics and finance from the Persian Gulf to the South China Sea. The rapid acceleration of the “internet of things”, to-date and to-come, forever moves semiconductors ahead of oil as the world’s key commodity input for growth. The current severe chip shortage halting automotive production underscores the speed and scale of this change. US firms lead the world in developing and selling semiconductors, accounting for 45% to 50% of global billings, but manufacturing has shifted to Asia – enough so for the US trade position to turn negative. Taiwan and Korea account for 83% of global processor chip production and 70% of memory chip output. The region’s lead will continue to expand with the increasing technical and capital intensity necessary for future semiconductor production.

"Like OPEC was for oil, Taiwan and Korea are near-monopoly producers of chips"

This structural shift to semis powers East Asian growth. Over the past five years chip sales accounted for an average 64% of annual Taiwanese export growth and 41% of Korea’s. The importance of semiconductor exports has only increased during the pandemic, total sales equaled 167% of Korea’s Jan-Sep current account surplus and 146% of Taiwan’s. We expect exceptionally strong demand to continue and remain overweight Korea and Taiwan equities.

With greater demand for semiconductors comes new geopolitical heft. Taiwan and Korea are on the front line of the US-China confrontation, reliant on China for growth, but on the US as guarantor of national security. Nevertheless, chip manufacturing dominance means they can leverage their increased strategic importance for economic and political gains. Recent wins include a new trade deal for Korea and weapon sales to Taiwan. The clearest market implication is in FX. Treasury placed Taipei on its currency manipulator watch list in December, but we believe Korea and Taiwan are too important for any meaningful action by the US and FX intervention will continue. Taipei and Seoul will do all they can to maintain the status-quo. As the Huawei saga showed, unless forced by hard power sanctions, they will not pick sides. They also plan to keep advanced manufacturing facilities in Asia. TSMC will open a US fab, but for low-end production only - Taipei understands the value of its “silicon shield”.

"Global growth is dependent on their output, and inflation on their prices"

The two biggest customers are China and the US, but they are different in many ways. While most chips purchased from Taiwan/SK are for final product, a good part of Taiwan’s production is for American chip firms, such as Nvidia, where designers choose less expensive places to produce: US volume of billings has soared, but employment has stayed flat (Chart 2). Although production location cannot shift quickly, production for strategically critical components is an issue for the US. In the defence bill just passed there was a provision for subsidizing US chip manufacturing and research, a counter to governmental subsidies in the Far East. The provision will be funded - there is bipartisan support, and it fits with Biden’s “build back better” program. Geopolitically, Trump dragged the chip industry into the middle of the US-China trade war and Pompeo re-recognized the Taiwan government. The Biden Administration will strengthen relations with SK and Taiwan, and likely use chips as leverage against China. But for now, in stark contrast with China, the US is comfortable with offshore production.

For Beijing, semiconductor dependence is a “knife at China’s throat”. Improving domestic innovation and technology self-reliance are its two top policy priorities for 2021. Beyond this year, ambitious ‘China 2025’ targets still hold. The near-term focus is de-Americanisation of technology supply chains, meaning import substitution where possible, and order rerouting to East Asia if it is not. But cutting out US suppliers further increases PRC reliance on Taiwan and Korea. Such is the Mainland dependence on Taiwan, that Beijing is unwilling to apply economic pressure to the island, instead China has adopted “grey zone” warfare tactics, and even talk of military action, all while continuing to purchase TSMC products.

"Chips are in the vortex of the US/China rivalry, and there they will stay"

For investors, semiconductor market value is today more rooted in fact than promise, compared to the 1999 dot-com bubble. Information technology had a weight of 6% in the S&P 500 in 1992, it rose to 30% at the peak of the dot.com bubble, subsequently fell and is now back up at 28%. There is no relation between weight and future performance, but we would argue the present is unlike 1999. Chips have moved well beyond consumer electronics, and are embedded either directly in all objects, or indirectly via the machines and processes that build them. Capex is now semiconductor intensive -- particularly “green” capex and next-generation infrastructure investment that is set to dominate government and private sector spending.

In sum, Taiwan and South Korea are the “new OPEC”: supply, demand and bottlenecks to global growth will revolve around Taiwan and SK chip production. They will not hold effective monopoly power over production forever, but their technology lead, R&D spending and capex plans preclude any change to the duopoly in at least the next five years. Shortages related to rapid upswings in demand could become inflationary, (TSMC is set to raise prices by 10-15%, the industry will follow) a sharp change for a product more known for steadily declining prices. Rising prices encourage competition but the barrier-to-entry remains high and if price spikes are managed, their global hegemony over chip production can remain in place for an extended period. And with that the balance and focus of geopolitics has changed. Not forever, but it will seem that way.