Client Login

Client Login Contact

ContactGlobal spread of the Covid-19 virus looks likely to cause a worldwide recession and bear market in stocks. Nobody knows how serious the disease is likely to be. But The Brookings Institution’s estimates suggest a reasonable likelihood that 10% of the US population will catch the virus, and of those at least 1% will die. As that implies more than 300,000 US deaths, personal fear is rational – there is more to fear than ‘fear itself’. (These estimates are not exaggerated: in the UK, for example, official sources have aired estimates of possible 60% incidence for the disease, not Brookings’s 10%. And the Brookings range for the mortality rate was 1-2%, though other analyses suggest rather under 1%.)

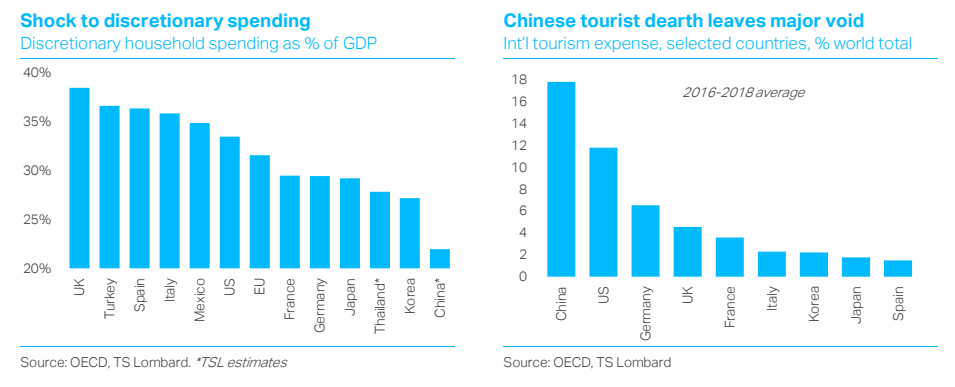

DM discretionary consumer spending is typically one third of GDP. Suppose it is cut 5% in Q2 – for Q1, any cuts in March may be offset by consumer hoarding of food and medical/household supplies. Then Q2 GDP will fall 1.7%, or an annual rate of 6½-7% in the US mode of presenting accounts. It could be more, it could be less – nobody knows, and there are no precedents. Such a Q2 decline would certainly spill over into Q3, reinforced by falling business capex and hobbling the nascent housing recovery. European reactions to the threat of Covid-19 are likely to be as strong as in the US – Italy is already in lock-down with thousands of cases and 366 deaths so far.

China, origin of the virus, was worst hit in Q1, in which real GDP almost certainly will have fallen. It seems to have contained the disease by draconian restrictions on movement. Migrant workers are now heading back to the factories, and the supply side should be back on track by the end of Q1 (ie, this month). A major infrastructure programme should cause some recovery during Q2 and H2, but the fear factor and weak exports (owing to recession elsewhere) could inhibit this.

US policy is unlikely to involve major fiscal action until unemployment is clearly rising, at which point tax cuts are likely. The Fed will eventually need to cut rates by another 50bp, but meanwhile needs to focus its QE-type re-investment programme at the very short end, to get short rates, and therefore bank funding costs, below the 2-year yield (now at 30bp) that typifies the rate of bank loans. This won’t be as effective as China’s mandated ‘forbearance’, but it’s all the Fed can do to encourage it – or at least not discourage it.

In Europe, China’s emphasis on manufacturing may help Germany, vis-à-vis France, the UK and Spain, but the recessions on average could match the US. Interaction of Italy’s Covid-19 lock-down with its precarious finances and weak banks could roil debt markets.

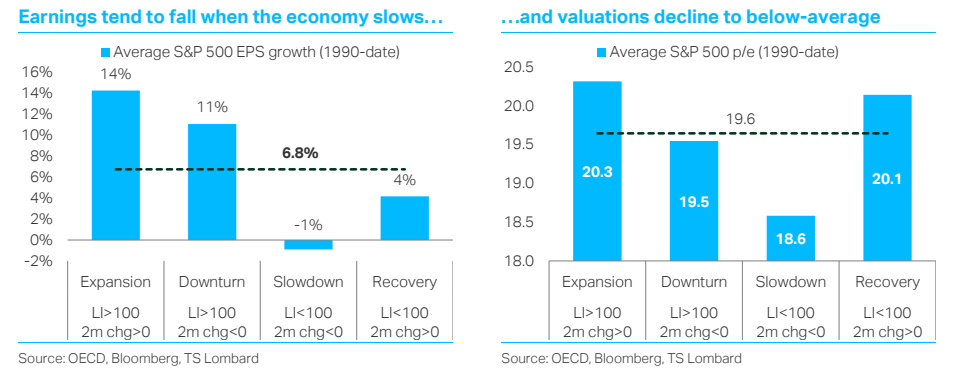

For stocks, we forecast the combination of negligible earnings growth this year with cuts in forward p/e ratios could take the S&P 500 down to the 2500 level, more than 25% down from its February 19th peak. The charts below support the view that earnings will at best stagnate, while the p/e ratio tends to be below average in Slowdown phases of the cycle. While the charts illustrate the post-1990 average, the results were significantly more bearish in the two recessions during the past 30 years: the tech bubble-burst (2000-02) and the great financial crisis (2007-09).