Client Login

Client Login Contact

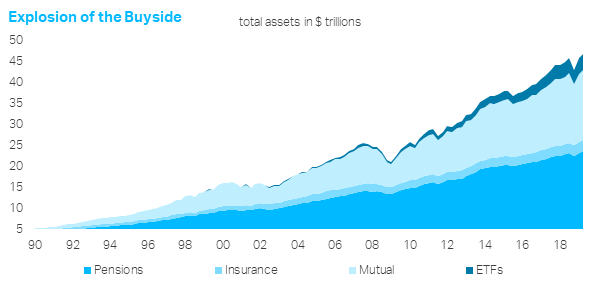

ContactBack in 2018, we warned about what we called the ‘Buy-side Bubble’. To the extent we could identify vulnerabilities in global markets, the clearest danger involved a powerful search for yield. Investors had naturally responded to a decade of low interest rates by seeking higher returns in riskier, longer-duration and more illiquid securities. The next financial crash would probably not be about large investment banks that had taken on too much leverage or funded themselves in dangerous ways, but it might see institutional investors play a pivotal role in the unwinding of this search for yield. The regulatory authorities had taken action to prevent a repeat of the subprime crash, but they seemed oblivious to risks in the asset-management industry.

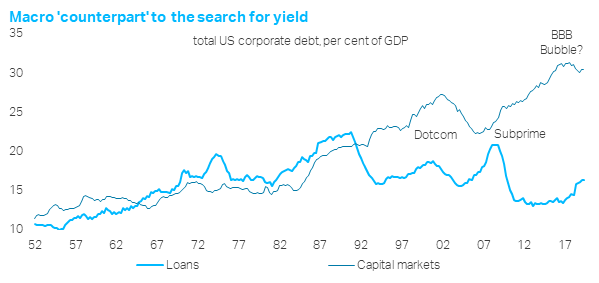

We explained how the insatiable appetite for yield among buy-side investors had become a critical source of funding for companies all over the world, pushing corporate debt to potentially dangerous levels. Much of this debt was denominated in USD. By early-2019, the consensus agreed, with corporate debt suddenly the ‘big risk’ to the global economy. Policymakers also started to pay attention. Various institutions, including the Federal Reserve, the BoE, the OECD and the IMF warned about these dangers with unusual candour.

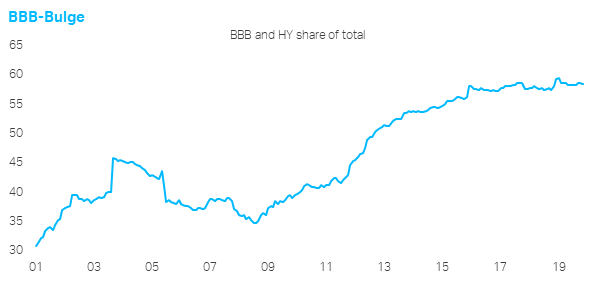

Corporate leverage has increased all over the world since 2012. While banks have generally scaled back their lending, capital markets have taken over. (China is the main exception to this theme, but even China’s bond market has played a more active role in the current cycle.) Internationally, corporate bond issuance has roughly doubled over the past decade and much of this has been concentrated in high-yield, or at the lowest end of the investment-grade spectrum (BBB).

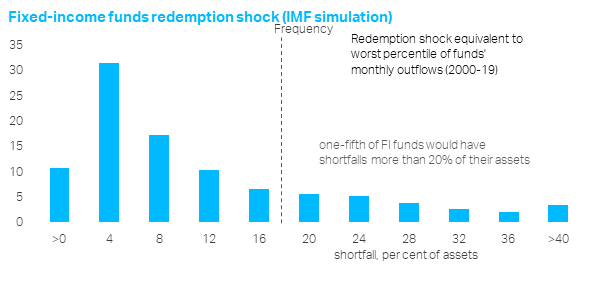

Our worry is that any sustained deterioration in the credit cycle could trigger an unprecedented wave of downgrades (fallen angels), which could overwhelm the junk bond market’s capacity to absorb them. Worse, some institutional investors might be forced to dump these securities, leading to ‘fire-sales’ of risky securities and an aggressive tightening in credit conditions. This risk is arguably most acute in the United States, which has been one of the main beneficiaries of the search for yield and has seen corporate debt ratios rise to record levels. While the aggregate balance sheet of American companies doesn’t look great, even this is flattered by a relatively small numbers of ‘superstars’. There is also a fat tail of weak companies.

In recent months, various industry insiders have tried to downplay the dangers associated with corporate debt and in particular BBB-rated bonds. They point out that some of the extra debt issuance has come from ‘non-cyclical’ sectors, such as healthcare, while companies are already taking action to address investor concerns – such as extending maturities or cutting their spending. Yet there is really no way of knowing how these credit markets will perform under serious stress conditions, particularly as liquidity has been deteriorating in recent years. Recent analysis from the Bank of England, the IMF and the BIS suggest there will be serious strains.

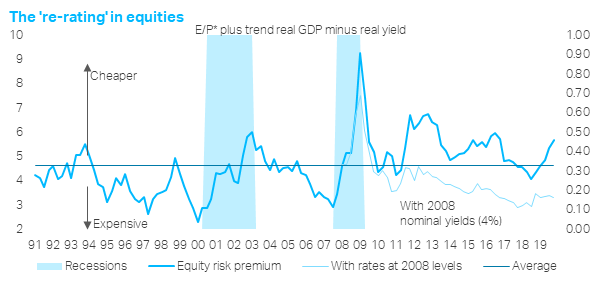

Perhaps the more important point is that policymakers – especially central banks – are now aware of these risks and will make every effort to keep interest rates down and extend the credit cycle. The hurdle for policy tightening has increased sharply, even in the unlikely scenario where inflation starts to rise. Profitability is now the more serious threat to corporate balance sheets, especially as earnings are already deteriorating. But even with sluggish productivity, we see only a modest squeeze on profit margins into 2020. This means, though the BBB-bomb will keep ticking, it should not explode anytime soon. The post-2009 expansion can continue.