Client Login

Client Login Contact

ContactThe breadth of the commodity rally started narrowing in early March, when the dust from Russia-Ukraine shock began to settle. Industrial metals topped out first and rolled over decisively in April – around the same time as the PBoC in effect set CNY on a path of accelerating depreciation. Agricultural prices turned lower in May, leaving energy to pull the cart. And negative momentum seeped into the energy market last month as the advance in oil prices ran out of steam.

Is this trend temporary or does it contain the seeds of a major downswing?

The mix of deficient output and thin inventories is bound to keep fundamental balances tight across the major commodities for the foreseeable future. The question going forward is how far demand will continue to expose these supply-side challenges.

Last year’s powerful economic upcycle was reinforced by the risk pendulum swinging wildly in the bullish direction. In other words, both physical demand (i.e., driven by economic activity) and financial demand (i.e., driven by money flows) moved together, keeping the fire under commodity prices going strong. Real demand was boosted by the post-Covid growth snapback in 2021 and later amplified by a rush to secure supplies spurred by the fallout from Russia’s invasion of Ukraine. Financial demand picked up, too, as investors sought exposure to commodities as a portfolio hedge against rising inflation, with speculative flows turbocharging the rally.

These positive dynamics climaxed in the spring; meanwhile, mounting concerns over a global economic recession are dampening the outlook for physical demand and pushing the risk pendulum in the bearish direction. As the world economy loses steam, demand for oil and other key commodities is more likely to cool than accelerate, albeit from high levels. The broad macro narrative is shifting from worries about protracted inflation to mounting fears of a global economic recession, brought on by combination of China’s slowdown with tightening global dollar liquidity (rates, QT, dollar) and a soft CNY. This has taken a toll on risk appetite, with credit spreads widening and equities coming under pressure.

Are commodities the “next shoe to drop”? The answer to that question needs to be nuanced.

Commodity prices are as good a coincident indicator of the global cycle as any: the cooling and subsequent reversal of the rally in 2022 Q2 is a tell-tale sign that the above-mentioned headwinds are starting to bite. This is the message from the price action – especially in copper and other key industrial metals, the most cyclically-sensitive commodities. Notably, the market was unimpressed by Beijing’s latest Covid policy tweak, which is consistent with our view that China’s domestic recovery looks set to remain weak and is therefore unlikely to counterbalance sluggish industrial momentum across the rest of the world economy.

Our take is that so far the price action reflects predominantly “financial” demand destruction as investors de-risk on escalating fears of a “hard landing” — fears that intensified following the Fed’s hawkish message in June. Speculative activity in the commodity futures markets shows an increasingly bearish tilt, while energy and mining stocks have suffered heavy losses since mid-June, underperforming the broader market.

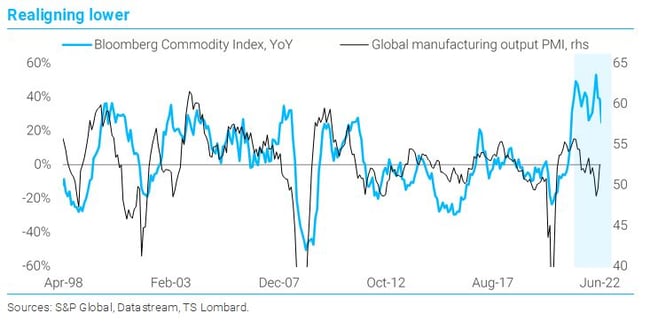

Just as the damage in global equities has been driven until now by multiple contraction, not falling earnings expectations, so a similar kind of dynamic applies to commodities: the “micro” fundamentals remain tight, but air is coming off the market as investors see the chances of severe physical demand destruction down the road rising – i.e., the macro and risk headwinds are getting stronger. For now, cooling commodity prices are “coming back down to earth”. They are retracing lower in tandem with US long yields and inflation breakeven rates. And they are aligning closer to the PMIs against the backdrop of cooling new orders and a maturing inventory cycle.

All eyes on crude. It looks as if only big negative demand surprises can kill this oil market. Near term, physical demand is bound to stay strong – not least in view of robust travel activity during the summer season after two years of Covid restrictions – although recent evidence of a slowdown in US gasoline demand suggests the market is cooling. US crude output is rising, yet OPEC+ is struggling to hit its increased output targets and commercial inventories are still low. Refining margins have come off in the last month but continue to be wide, translating into an incentive to bid up crude. Meanwhile, the lingering threat of Putin “weaponizing” Russia’s energy sources is set to keep volatility elevated. Overall, this remains a broadly constructive mix for crude prices, albeit with tentative signs of upside exhaustion that point to a more pronounced “two-way” market during the summer.

All eyes on crude. It looks as if only big negative demand surprises can kill this oil market. Near term, physical demand is bound to stay strong – not least in view of robust travel activity during the summer season after two years of Covid restrictions – although recent evidence of a slowdown in US gasoline demand suggests the market is cooling. US crude output is rising, yet OPEC+ is struggling to hit its increased output targets and commercial inventories are still low. Refining margins have come off in the last month but continue to be wide, translating into an incentive to bid up crude. Meanwhile, the lingering threat of Putin “weaponizing” Russia’s energy sources is set to keep volatility elevated. Overall, this remains a broadly constructive mix for crude prices, albeit with tentative signs of upside exhaustion that point to a more pronounced “two-way” market during the summer.

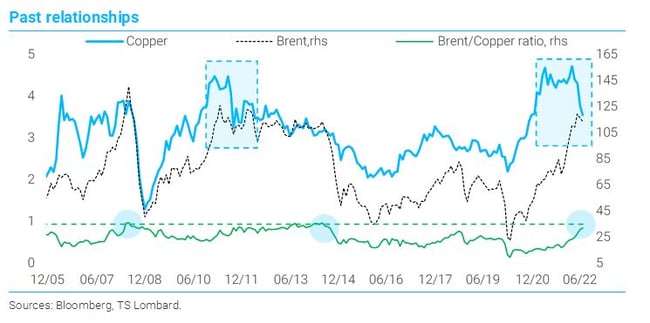

We note that the Brent/copper ratio is now not far from levels that have marked major turning points for commodity prices in the post-GFC era. A closer look at that the chart below also shows a double-top formation in copper prices (2021 H1–2022 H1) that is reminiscent of 2011 – like now, a time of dollar appreciation (albeit from a much lower level) and deteriorating industrial momentum. Back then, copper’s behaviour foreshadowed a period of range-bound oil prices; so, if history is any guide, this seems to reinforce our view that the chances are oil prices will cool in the near term.

Persistent stagflationary global macro dynamics are set to weigh on the global demand outlook but also keep DM central banks willing to err on the side of hawkishness. As with equities, in this environment the chances are that the commodity market is likely to get worse before it gets better. The burden of proof is increasingly with the bulls.

Persistent stagflationary global macro dynamics are set to weigh on the global demand outlook but also keep DM central banks willing to err on the side of hawkishness. As with equities, in this environment the chances are that the commodity market is likely to get worse before it gets better. The burden of proof is increasingly with the bulls.