Client Login

Client Login Contact

ContactAn effective COVID-19 vaccine is great news because it will save lives and means we might still escape from the current economic crisis with minimal long-term scarring.

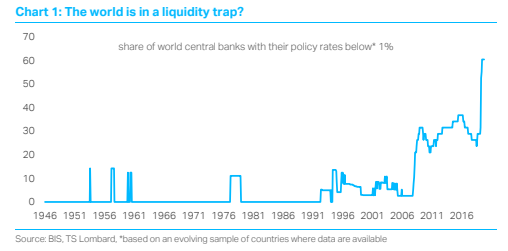

Yet, the global economy faces a difficult winter, with accelerating infection rates and a double-dip recession. Investors are wondering what the authorities could do revive their economies, especially if growth remains disappointing once the pandemic is over. Even the IMF is worried, with Gita Gopinath saying the world is now in a liquidity trap. While it is unusual for the IMF to issue such a blunt warning, this is not surprising given the nature of the COVID recession and the experience of the last decade. Conventional monetary policy, based on reducing interest rates, has now run its course. Even if central banks had room to cut rates further – they don’t, because they know NIRP is dangerous – low borrowing costs would not help those sectors that are suffering most. Meanwhile, the IMF’s warning should remind investors about the ineffectiveness of QE. There is nothing magical about the combination of QE and budget deficits. This policy mix is not “effectively monetary financing”. While true helicopter money would be a solution to the liquidity trap, today’s combination of fiscal and monetary stimulus is only reflationary to the extent the fiscal part of this package is large enough to plug the hole in private demand. Right now, it isn’t.

To meet their inflation mandates, central banks are desperately hoping for more support from fiscal policy. There is a strong consensus among economists that this will be necessary, including over the medium-term to combat persistent secular stagnation. But what if the politicians fail to deliver, or return to austerity too quickly after the virus has passed? Is there anything more central banks can do, or will they have to resign themselves to never hitting their objectives? The short answer is that they can do more, but only if they are prepared to cross the boundary between fiscal and monetary policy. They would do this by engaging in activities that would damage their balance sheets, destroying their “equity”. Unlike commercial enterprises, the “net worth” of a central bank should not matter – these institutions cannot become bankrupt and they can always create new zero-interest liabilities to fund themselves (i.e. “print money”). Inflation is their only genuine constraint, as MMT rightly points out. Yet, the more important point about central banks running large losses is that their actions will have a direct impact on the public finances, either through reduced revenues for the Treasury or, in some jurisdictions, necessary recapitalization (an immediate fiscal cost). While an inflation-targeting central bank will never monetize government spending, it can decide when/how the government "pays for it".

" Central banks can do more, but only if they are prepared to cross the boundary between fiscal and monetary policy. "

What does this mean for the current situation? Obviously, central banks are reluctant to go deeper into quasi-fiscal space. They would much rather elected officials provided the necessary stimulus (i.e. plain vanilla fiscal policy, set according to wider government objectives). But they still have a variety of “nuclear options”, which they could pursue with the blessing of their political masters. The least controversial idea would be a radical version of what the ECB is already doing, using “dual interest rates” to inject cash into the economy. Make no mistake, paying banks a fee to provide cheap loans (or even “free money”) to households and businesses is not a good way to conduct fiscal policy, but it might be acceptable to bureaucrats who are used to dealing only with other financial institutions. Alternatively, central banks could create more transparent cash transfers, either directly to government accounts or – more likely – via the creation of new digital central bank currency (CBDC). China has already introduced a small “trial” version of this, though there are implementation barriers in other jurisdictions. We think investors should rule nothing out, especially if there isn’t a full vaccine-induced recovery in the second half of 2021. While you have to wonder whether it is desirable for unelected officials to make decisions with clear distributional effects (who do they represent?), they have already been moving in this direction.

Read more blogs by Dario Perkins, Managing Director, Global Macro