Client Login

Client Login Contact

ContactCentral banks across the world have pivoted to a more hawkish mode in recent weeks. While this is in part acknowledgement that the recovery from COVID is continuing – albeit more hesitantly than officials expected at the start of the year – it also reflects growing anxiety about inflation. The following extract from the Bank of England’s latest policy deliberations sums up the mood: “Continuing with asset purchases when CPI inflation was above 3% and the output gap was closed might cause medium-term inflation expectations to drift up further. A decision to curtail the asset purchase programme at this meeting would… demonstrate the Committee’s commitment to returning inflation to target in the medium term and ensure that inflation expectations remained well anchored.” There are two big problems with this statement. First, it shows that officials still believe in the “expectations fairy”, even though there is no actual evidence it exists1. Second, it is not obvious why ceasing to swap one zero-interest government liability for another (i.e., ending QE) is supposed to scare the fairy away (if it does indeed exist). This just seems like the usual central banker nonsense. But there is a genuine inflation threat out there.

Before we start, let’s be clear that we are talking about the risk of more persistent inflation. Much of the inflation we see today still has a strongly “transitory” feel to it. This does not mean the price increases that have occurred in 2021 will reverse, only that prices will stop rising as quickly, so that inflation (the rate of change in the CPI) will drop back quickly in 2022 – even without a policy response. Nobody should understate the seriousness of the squeeze on real incomes. The pandemic has caused severe supply bottlenecks, global logistical chaos and various “reopening” costs for businesses that should eventually settle down, assuming the world can eventually escape from this crisis. But this last part, of course, is the big assumption everyone is making. What if the pandemic lingers into 2022 and these supply disruptions do not end quickly? Perhaps vaccine efficacy fades (requiring ongoing booster campaigns), or the virus mutates into something nastier, or those countries that have fallen behind in their vaccine deployment have to resort to new rounds of lockdowns, either in the winter or next year. This is surely a more serious and “real” threat to central banks’ inflation projections than anything the expectations fairy can muster.

Before we start, let’s be clear that we are talking about the risk of more persistent inflation. Much of the inflation we see today still has a strongly “transitory” feel to it. This does not mean the price increases that have occurred in 2021 will reverse, only that prices will stop rising as quickly, so that inflation (the rate of change in the CPI) will drop back quickly in 2022 – even without a policy response. Nobody should understate the seriousness of the squeeze on real incomes. The pandemic has caused severe supply bottlenecks, global logistical chaos and various “reopening” costs for businesses that should eventually settle down, assuming the world can eventually escape from this crisis. But this last part, of course, is the big assumption everyone is making. What if the pandemic lingers into 2022 and these supply disruptions do not end quickly? Perhaps vaccine efficacy fades (requiring ongoing booster campaigns), or the virus mutates into something nastier, or those countries that have fallen behind in their vaccine deployment have to resort to new rounds of lockdowns, either in the winter or next year. This is surely a more serious and “real” threat to central banks’ inflation projections than anything the expectations fairy can muster.

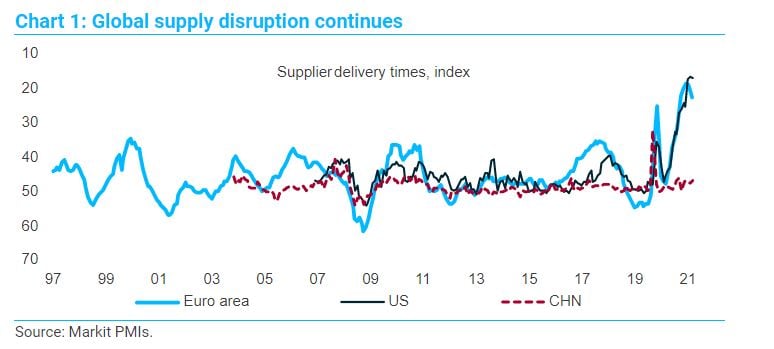

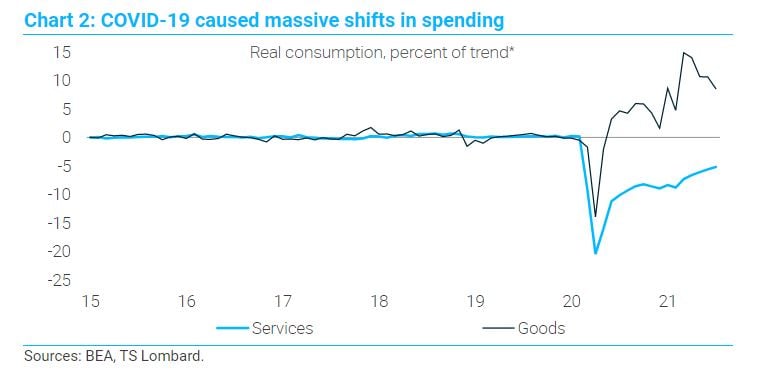

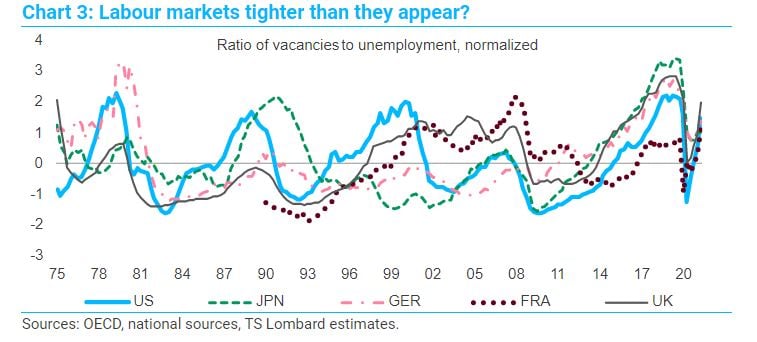

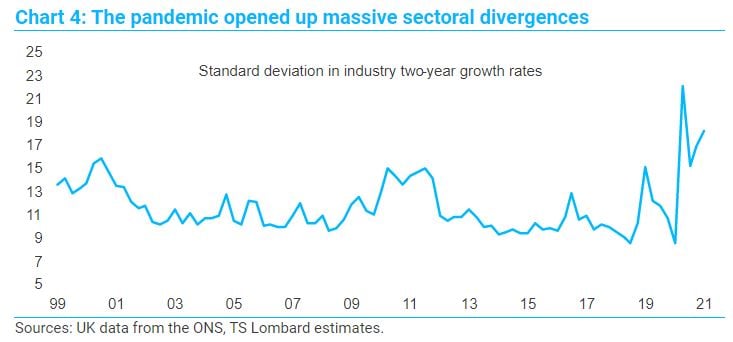

Economists love to think about inflation – like everything else in life –as the balance between demand and supply. But during the last 18 months, it has been the composition of economic activity that has had the more powerful bearing on global CPIs. We see this on two levels. First, COVID-19 caused massive shifts in the way people spend – the demand for services slumped (nobody wanted to sit in a restaurant or get a haircut) but the demand for goods surged. In aggregate, this raised prices because goods prices are more flexible and because costs are generally “convex”, which means strong goods demand raises the CPI more than weak services demand erodes it. Combine booming world trade (which had recovered fully from COVID even before the end of 2020) with various supply bottlenecks and shortages and you get a large spike in the CPI. The second inflationary impact from the pandemic is that it made most economies less efficient at allocating resources. We see this most clearly in labour markets, where serious “mismatch” has appeared. The coexistence of large numbers of unfilled job vacancies and high levels of unemployment (or millions of people on furloughs) suggests the jobs market is not working as effectively as it used to. In a long-since “cancelled” view of the labour market, this would have raised the NAIRU.

Economists love to think about inflation – like everything else in life –as the balance between demand and supply. But during the last 18 months, it has been the composition of economic activity that has had the more powerful bearing on global CPIs. We see this on two levels. First, COVID-19 caused massive shifts in the way people spend – the demand for services slumped (nobody wanted to sit in a restaurant or get a haircut) but the demand for goods surged. In aggregate, this raised prices because goods prices are more flexible and because costs are generally “convex”, which means strong goods demand raises the CPI more than weak services demand erodes it. Combine booming world trade (which had recovered fully from COVID even before the end of 2020) with various supply bottlenecks and shortages and you get a large spike in the CPI. The second inflationary impact from the pandemic is that it made most economies less efficient at allocating resources. We see this most clearly in labour markets, where serious “mismatch” has appeared. The coexistence of large numbers of unfilled job vacancies and high levels of unemployment (or millions of people on furloughs) suggests the jobs market is not working as effectively as it used to. In a long-since “cancelled” view of the labour market, this would have raised the NAIRU.

If the pandemic winds down, as the consensus is still assuming, most of these issues should resolve themselves. Supply will respond to higher prices, while consumers will substitute “stuff” for “experiences”, easing the pressures on global industry. The flexibility of goods prices – a source of inflation in 2021 – should become a source of disinflation. Historically, this has always been the case. And as fiscal support diminishes (especially via unemployment insurance), fear of the virus fades and the schools reopen (allowing working parents to re-enter the jobs market), people should return to work and the mismatch in labour markets should disappear. Yet there are still big question marks about all of this, especially in terms of how far and how quickly the world’s major economies will need a reallocation of resources. If, for example, the problems in labour markets reflect a mismatch of vacancies and people across sectors and geographical regions, they might persist. What if we now need fewer waiters and more cloud-computing experts? Or maybe working from home will mean big cities like New York and London continue to struggle. Companies in high-demand areas might be forced to raise wages in what might well be a futile effort to attract staff from other parts of the country. That is not to say the world won’t eventually adjust, but the adjustment could take longer than people realize.

If the pandemic winds down, as the consensus is still assuming, most of these issues should resolve themselves. Supply will respond to higher prices, while consumers will substitute “stuff” for “experiences”, easing the pressures on global industry. The flexibility of goods prices – a source of inflation in 2021 – should become a source of disinflation. Historically, this has always been the case. And as fiscal support diminishes (especially via unemployment insurance), fear of the virus fades and the schools reopen (allowing working parents to re-enter the jobs market), people should return to work and the mismatch in labour markets should disappear. Yet there are still big question marks about all of this, especially in terms of how far and how quickly the world’s major economies will need a reallocation of resources. If, for example, the problems in labour markets reflect a mismatch of vacancies and people across sectors and geographical regions, they might persist. What if we now need fewer waiters and more cloud-computing experts? Or maybe working from home will mean big cities like New York and London continue to struggle. Companies in high-demand areas might be forced to raise wages in what might well be a futile effort to attract staff from other parts of the country. That is not to say the world won’t eventually adjust, but the adjustment could take longer than people realize.

I have explored this downside scenario in one of my research publications. It is the “VILE macro regime”, a world of Volatile Inflation and Limited Expansion. Tighter monetary policy is not a solution, but it is a backdrop that creates serious dilemmas for policymakers – because they essentially face a deterioration in the mix between GDP and inflation. Central banks are probably wrong to assume more volatile (or even slightly stickier) inflation will automatically generate a nasty wage-price spiral – this is not the 1970s – but you can understand why they are becoming a little more concerned about recent price trends. It is to be hoped that the authorities will treat “inflation expectations” the same way they treat “macro-prudential policy”, using verbal interventions (i.e., sounding more hawkish) as a substitute for actually doing anything about it. But the hurdle for ending QE is a lot lower than for raising interest rates. Even central bank officials must be wondering why they are still doing QE, 18 months after it stopped being useful. Put all this together – more volatile inflation, weaker global growth and no QE – and you get a trickier market backdrop, too. Even “old” risks like China’s debt imbalances start to matter again.

I have explored this downside scenario in one of my research publications. It is the “VILE macro regime”, a world of Volatile Inflation and Limited Expansion. Tighter monetary policy is not a solution, but it is a backdrop that creates serious dilemmas for policymakers – because they essentially face a deterioration in the mix between GDP and inflation. Central banks are probably wrong to assume more volatile (or even slightly stickier) inflation will automatically generate a nasty wage-price spiral – this is not the 1970s – but you can understand why they are becoming a little more concerned about recent price trends. It is to be hoped that the authorities will treat “inflation expectations” the same way they treat “macro-prudential policy”, using verbal interventions (i.e., sounding more hawkish) as a substitute for actually doing anything about it. But the hurdle for ending QE is a lot lower than for raising interest rates. Even central bank officials must be wondering why they are still doing QE, 18 months after it stopped being useful. Put all this together – more volatile inflation, weaker global growth and no QE – and you get a trickier market backdrop, too. Even “old” risks like China’s debt imbalances start to matter again.

1 At least one Fed official has now seen the light, having a full Jerry Maguire style “it’s a breakthrough not a breakdown” moment in a paper he published last week on the uselessness of inflation expectations. He should have called it “Things we think but do not say”, a reference to Jerry’s famous outburst.